Unit root (DickeyFuller) and stationarity tests on time series

KPSS is another test for checking the stationarity of a time series. The null and alternate hypothesis for the KPSS test are opposite that of the ADF test. Null Hypothesis: The process is trend stationary. Alternate Hypothesis: The series has a unit root (series is not stationary). A function is created to carry out the KPSS test on a time series.

(PDF) Improving the empirical size of the KPSS test of stationarity

Abstract. In this paper, we generalize the KPSS-type test to allow for two structural breaks. Seven models have been defined depending on the way that structural breaks affect the time series.

(PDF) The KPSS test with outliers

Lina Sjösten Bachelor's thesis in Statistics Advisor Yukai Yang 2022 Abstract This thesis investigates through simulation why tests of unit root and stationarity occasionally result in different conclusions. The thesis focusses on the KPSS test and the ADF test and both review cases with and without a trend.

(PDF) A bootstrapbased KPSS test for functional time series

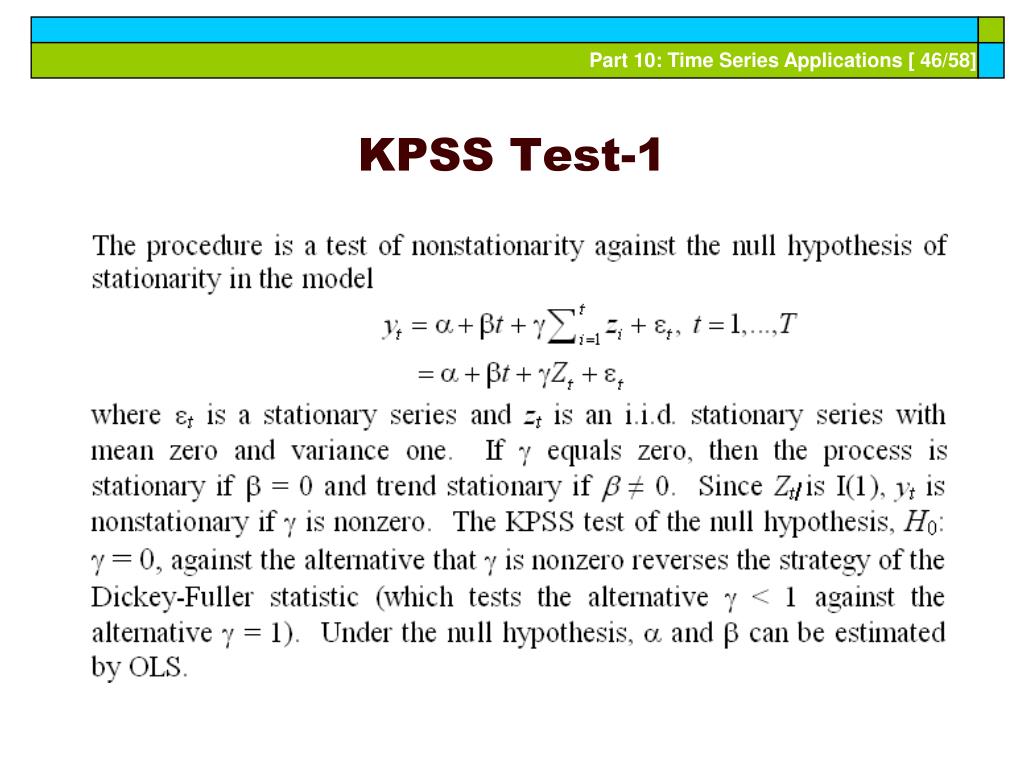

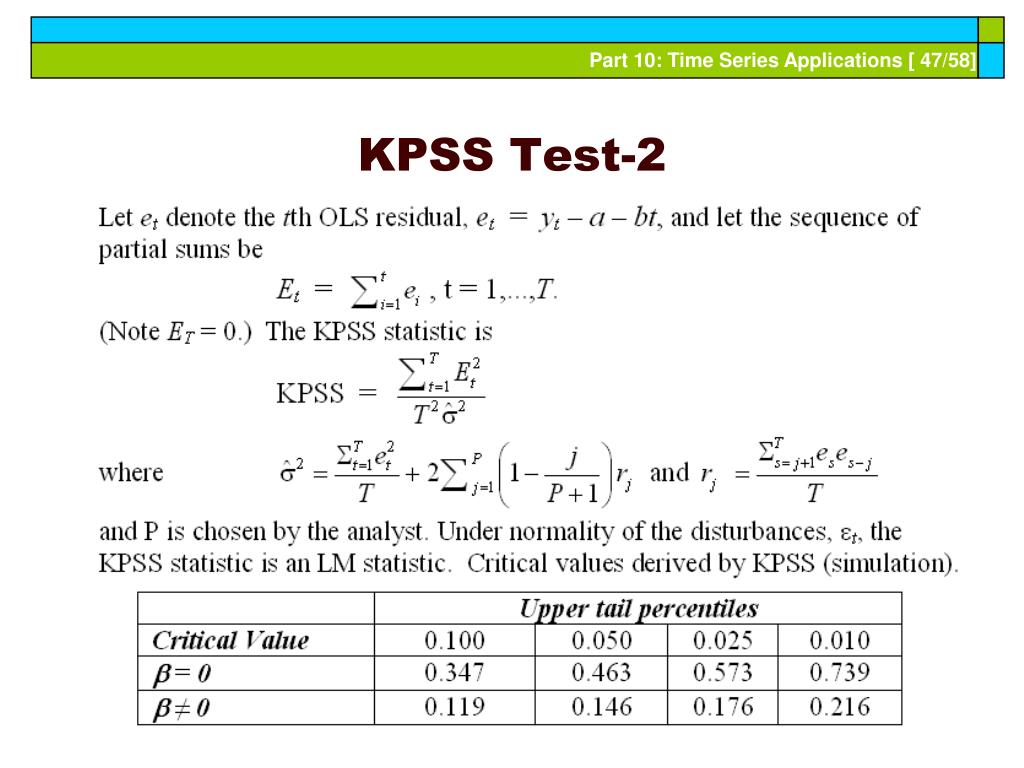

The model considered by KPSS is a special case of the regression model in Nabeya and Tanaka (1988): y, =xtßt +z'tY +et, ßt = ßt—ι + ut ι where xt and zt are nonstochastic sequences, and they suggest the one-sided LM test statistic (this is the same as the LBI test) for Hq : σΐ/σε2 = 0, against H\ : /σ^ > 0,

(PDF) The KPSS test with two structural breaks

The KPSS test, short for, Kwiatkowski-Phillips-Schmidt-Shin (KPSS), is a type of Unit root test that tests for the stationarity of a given series around a deterministic trend. In other words, the test is somewhat similar in spirit with the ADF test. A common misconception, however, is that it can be used interchangeably with the ADF test.

KPSS VZOREC eDemenca

To test for a using the ADF test, one estimates the following model: 1 −1. first differences 2 ᄏ䅫+ ∑ ii=1 approximate the ARMA dynamics of the time series, β0 is a constant, and t is a trend. If the series has a unit root, β1 = 0 and hypothesis that β1 = 0 given n lagged first differences. =1. The ADF test is a test of the.

Unit Root Tests KPSS in Levels and First Difference Download

We propose automatic generalizations of the KPSS‐test for the null hypothesis of stationarity of a univariate time series. We can use these tests for the null hypotheses of trend stationarity, level stationarity and zero mean stationarity. We introduce the asymptotic null distributions and we determine consistency against relevant nonstationary alternatives.

Results of KPSS test. Download Table

The KPSS test As an alternative to the Dickey-Fuller style tests for stationarity, we may consider the KPSS test of Kwiatkowski, Phillips, Schmidt and Shin (J. Econometrics, 1992). This test (and those derived from it) have the more "natural" null hypothesis of stationarity (I(0)), where a rejection indicates non-stationarity (I(1) or I(d)).

(PDF) The Power of the KPSSTest for Cointegration when Residuals are

The test proposed in Kwiatkowski et al. (1992), often referred to as the Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test, has been used most extensively to test for stationarity of a time series. It relies on cumulation of squared partial sums of the demeaned and/or detrended series with a correction for autocorrelation using a.

PPT Econometric Analysis of Panel Data PowerPoint Presentation, free

This paper extends the KPSS test to the setting of functional time series. We develop the form of the test statistic, and propose two testing procedures: Monte Carlo and asymptotic. The limit distributions are derived, the procedures are algo- rithmically described and illustrated by an application to yield curves and a simulation study.

KPSS testinin yeni hali ve örnek sorular

In econometrics, Kwiatkowski-Phillips-Schmidt-Shin (KPSS) tests are used for testing a null hypothesis that an observable time series is stationary around a deterministic trend (i.e. trend-stationary) against the alternative of a unit root. [1]

Upper tail critical values for the KPSS test statistic asymptotic

In this study, we examine bootstrap methods to construct a generalized KPSS test for functional time series. Bootstrap-based functional testing provides an intuitive and efficient estimation of.

KPSS Testleri PDF

ADF test is very powerful in time series with outliers, but KPSS test should use with second thoughts in presence of outliers. The similar results are also reported by Otero and Smith (2005) .

How to Perform a KPSS Test in R (Including Example) Statology

similar to the KPSS statistic must be normalized by the long run variance rather than by the sample variance. We develop extensions of the KPSS test to time series of curves, which we call functional time series (FTS). Many nancial data sets form FTS. The best known and most extensively studied data of this form are yield curves.

ADF and KPSS Tests Results Intercept Intercept and Trend p ADF k KPSS p

The KPSS test is now widely used in empirical work to test trend stationarity and works as a complement to standard unit root tests in analyzing the properties of time series data.

PPT Econometric Analysis of Panel Data PowerPoint Presentation, free

What is the KPSS Test? The Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test figures out if a time series is stationary around a mean or linear trend, or is non-stationary due to a unit root. A stationary time series is one where statistical properties — like the mean and variance — are constant over time.